The capital-freeze index

Stop signs

Which emerging markets are most vulnerable to a freeze in capital inflows?

Sep 7th 2013/The capital-freeze index

- OVERALL

- Current acc.

- Debt

- Credit

- Openness

- Currencies

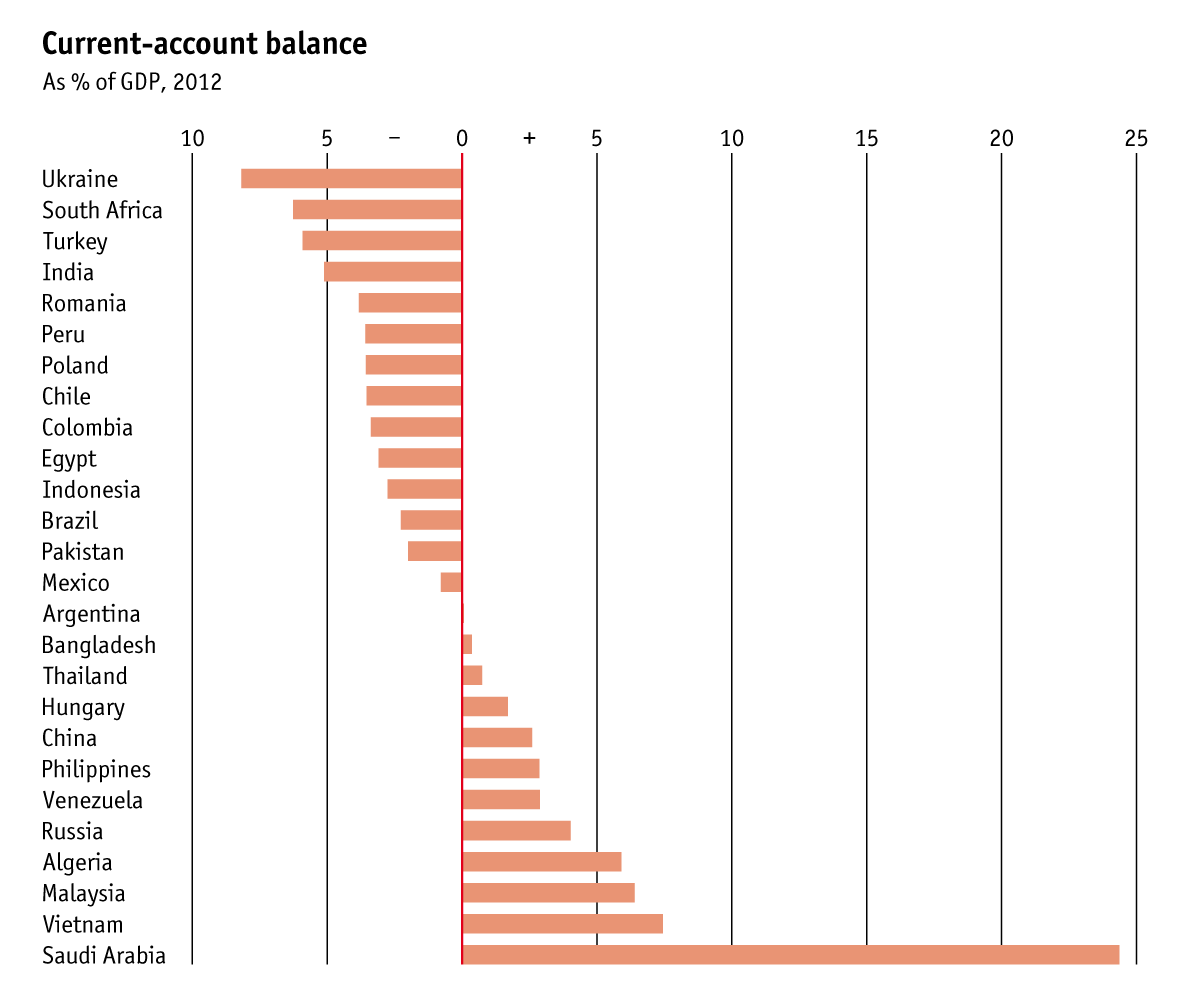

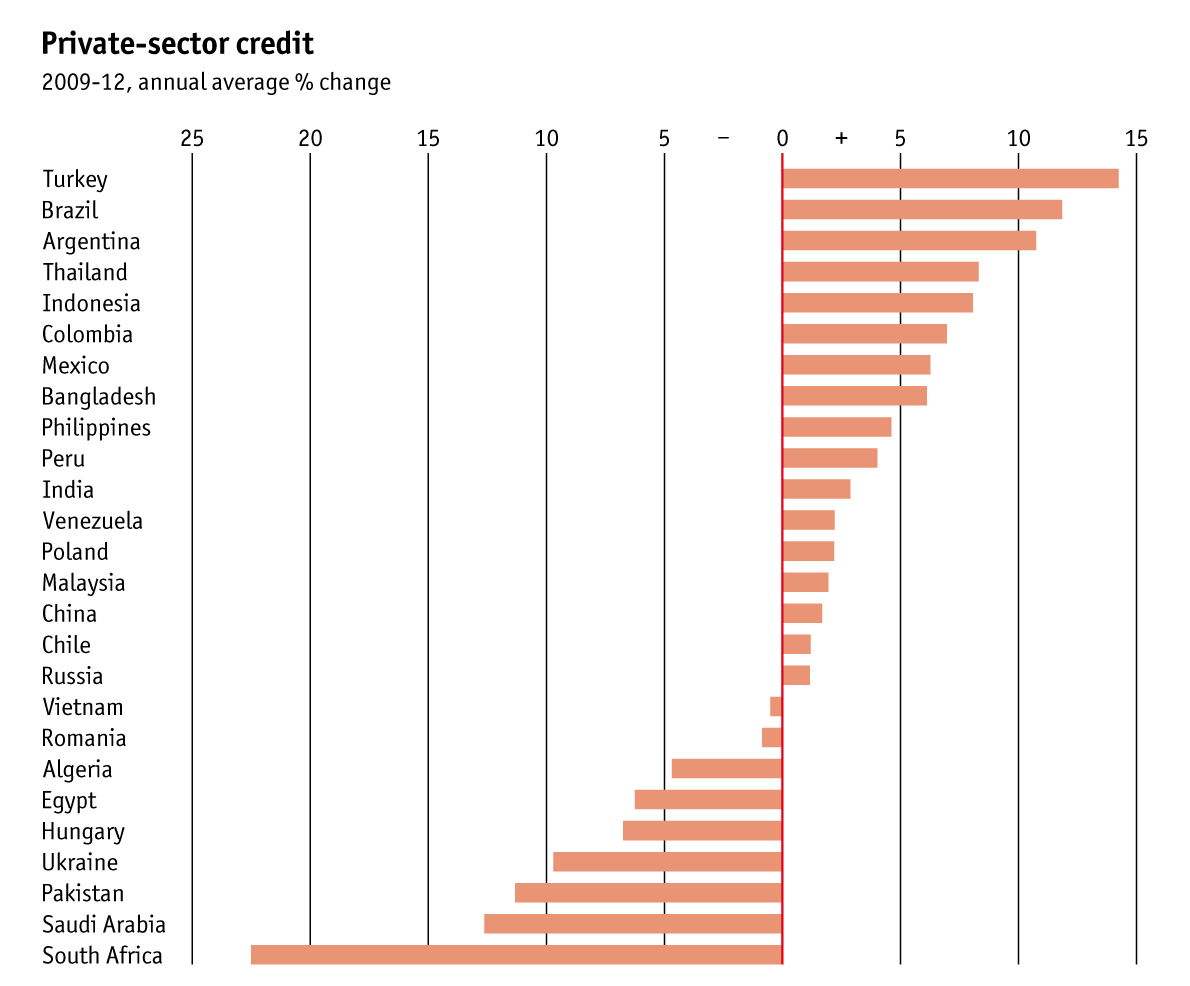

THE risk of an abrupt end to capital inflows is now a worry for much of the emerging world. Some places are more vulnerable than others. A large current-account gap implies lots of net borrowing from abroad, which could presage a credit crunch if funding dries up. A high level of short-term external debt relative to a government’s stock of reserves means an economy lacks the means to tide borrowers through temporary difficulties. Rapid credit growth often signals overstretched firms and overvalued asset prices. A more open financial system may boost growth in the long run, but it also makes it easy for capital to flood out fast.

The Economist has combined these four factors into an index measuring the vulnerability of 26 emerging markets to a capital freeze. We have used a simple traffic-light system to group the countries. Green denotes economies, including reserve-rich oil states, that are at relatively little risk from a sudden stop. A current-account surplus, a vast hoard of reserves and a closed capital account mean that whatever troubles befall China, they are unlikely to include a panicked flight of capital.

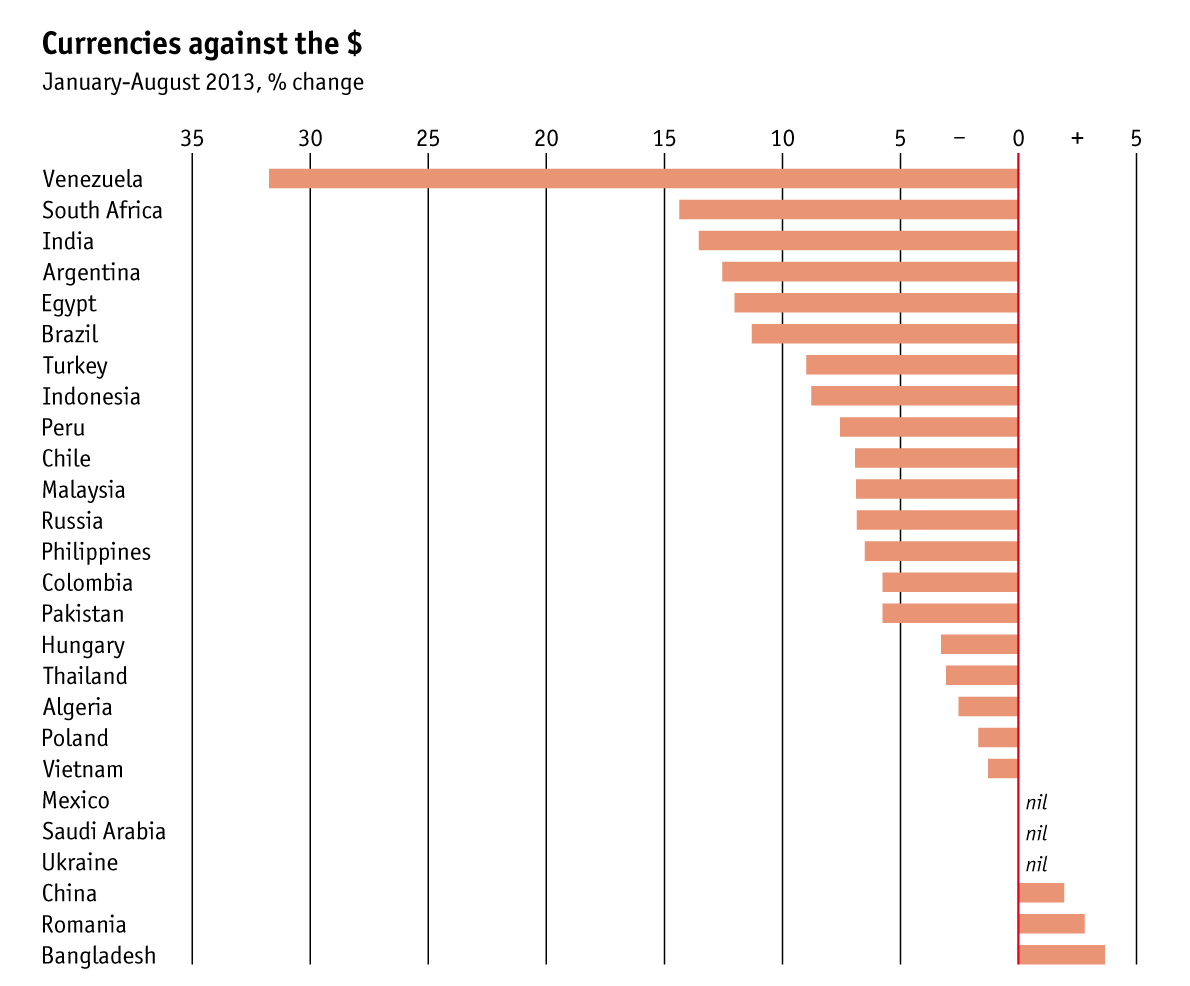

Many of the emerging world’s bigger economies lie in amber territory. India and Indonesia are already feeling the pressure. Others, like Mexico, have fared well amid recent turmoil: the peso has been roughly flat over the past year. But credit growth and high levels of financial openness are potential points of fragility. Malaysia and the Philippines, victims of the Asian crisis of the late 1990s, are in better shape now. Both run current-account surpluses and have built up a much larger reserve buffer relative to short-run external obligations. Yet credit growth has also been zesty.

Countries in the red zone are most at risk. South Africa, Ukraine and a clutch of Latin American countries all look vulnerable, but Turkey tops the list. It is running a current-account deficit of over 6% of GDP, its short-term external debt and debt payments amount to over 150% of available reserve assets, and since 2009 credit has grown faster there than it has in any other emerging market in the index. The Turkish lira has already fallen by 13% against the dollar since the start of the year, but it may yet sink further.

Δεν υπάρχουν σχόλια:

Δημοσίευση σχολίου